24 Mar 2026

Share on:

What is the milk market outlook in February 2026?

What was the global trend in milk production?

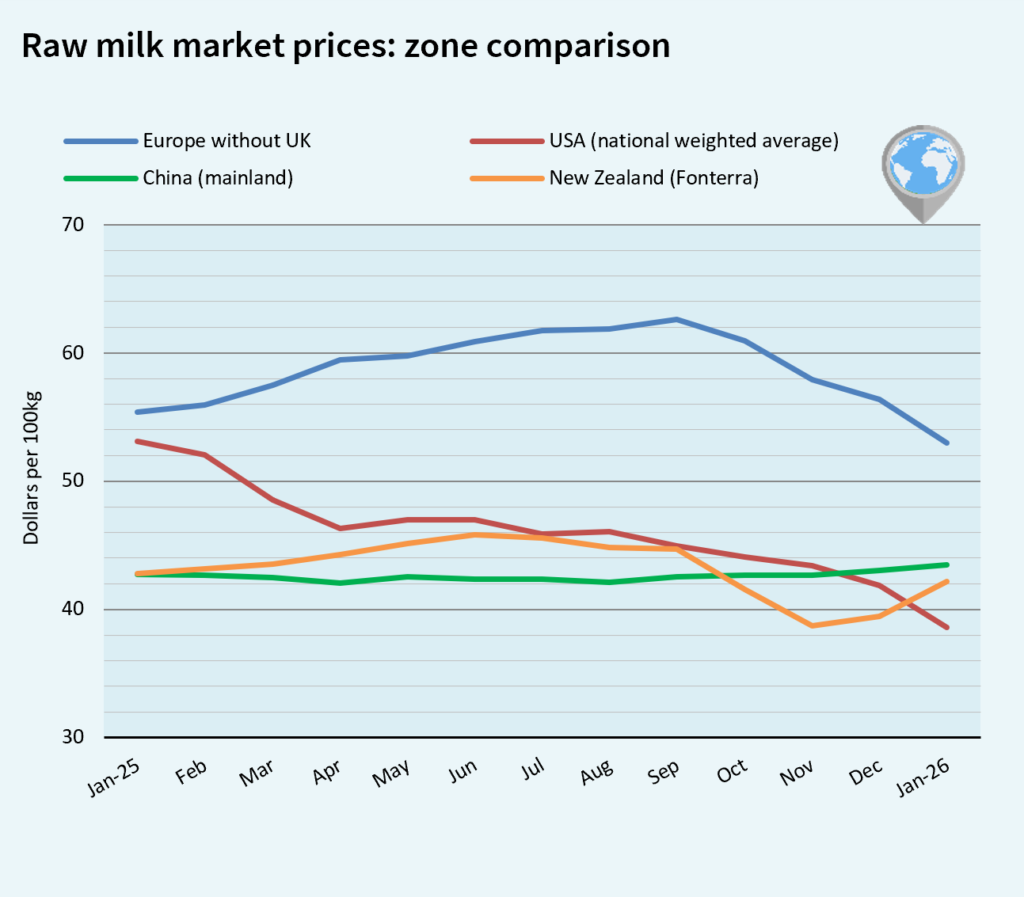

The Milk Market Outlook for February 2026, based on January 2026 data, shows that milk production is increasing in most major exporting regions, while farmgate prices are under pressure. Commodity prices are starting to rebound, especially in New Zealand, and China continues its gradual dairy sector recovery. This report summarizes trends country by country to help producers and market participants understand global market dynamics.

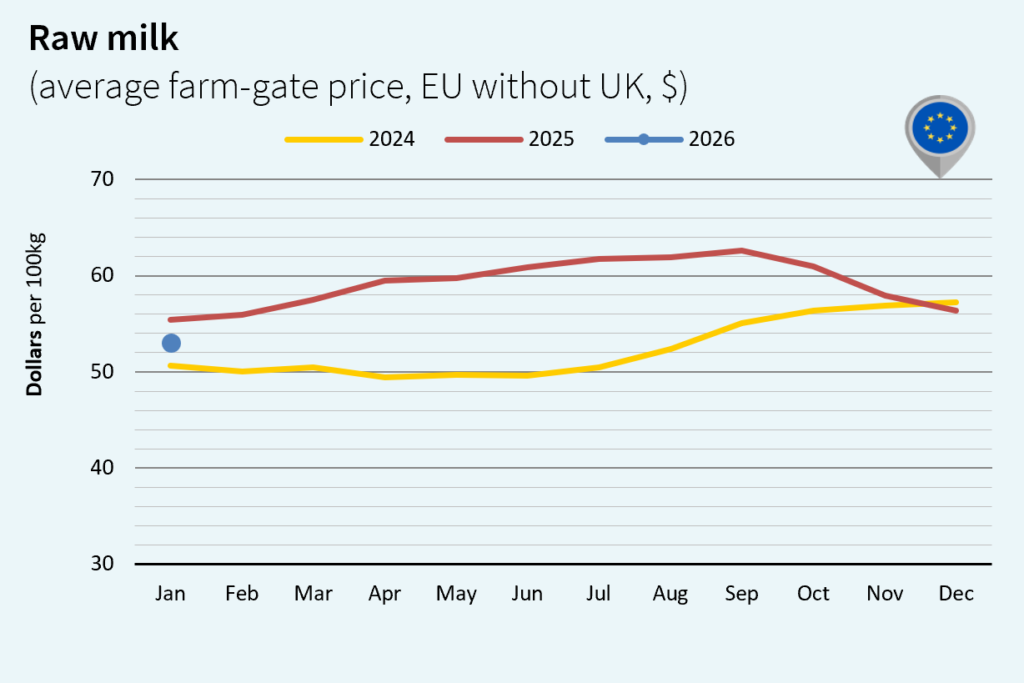

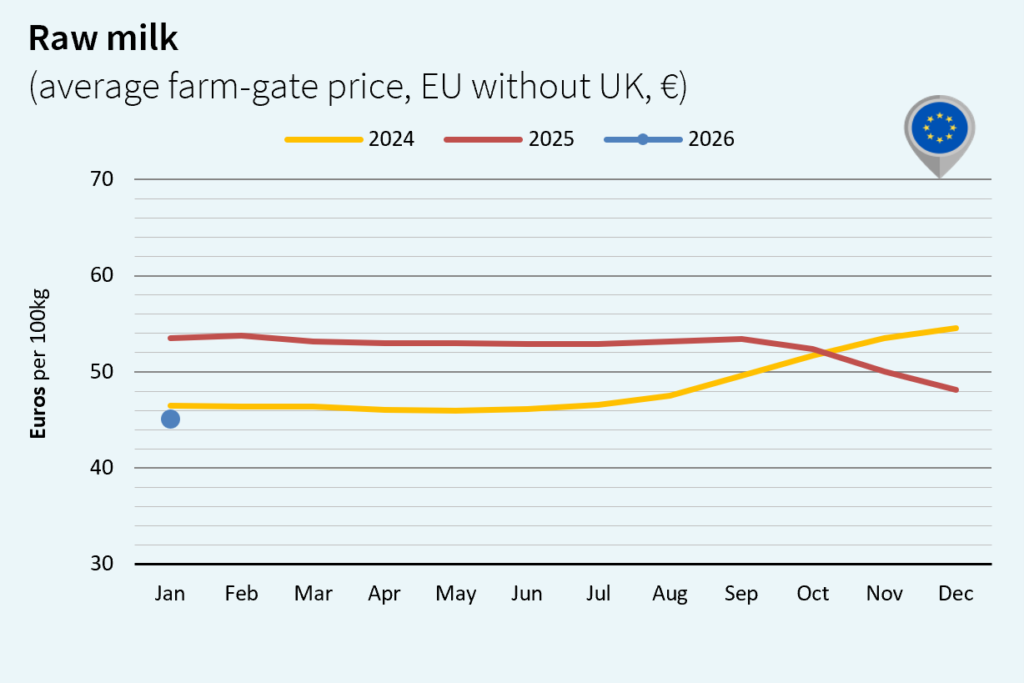

What are the latest trends in European Union milk production?

In January 2026, despite a slight slowdown in pace, year-on-year growth in EU milk production remained strong. It reached 12.14 million tons (+4.3% or +503,000 tons vs. 2025). Milk collections were still increasing across all major European exporters, while farmgate prices were declining. On average, the EU price reached US$53.00/100 kg (-6.0% vs. December 2025 and -4.3% vs January 2025).

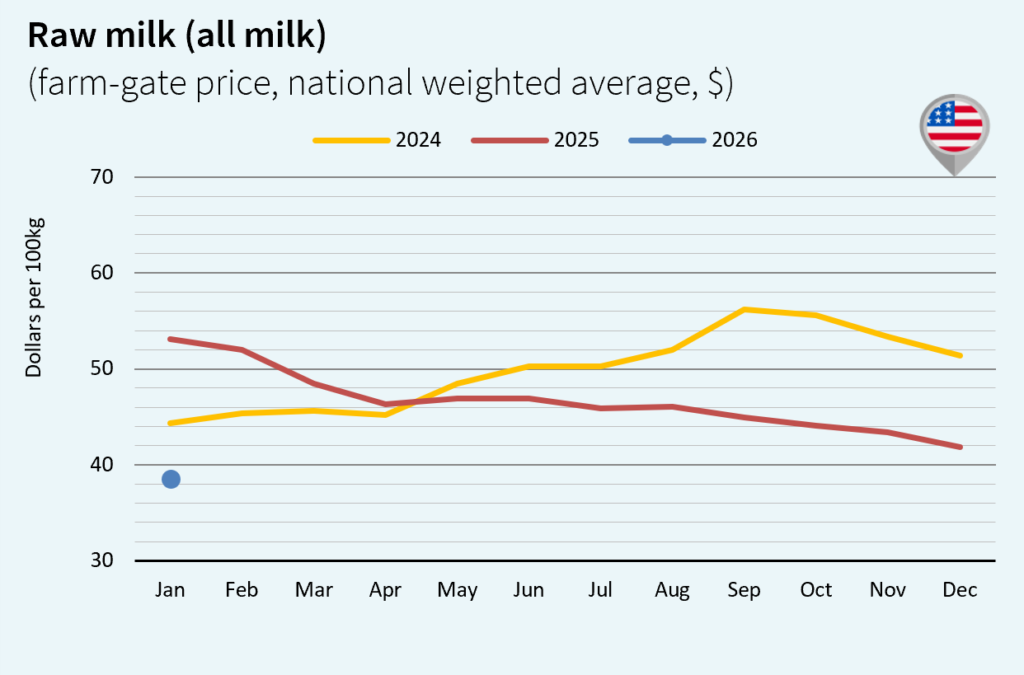

Which factors are affecting US milk prices?

In the US, the feed margin calculated by the USDA under its Dairy Margin Coverage (DMC) program has been declining for several months. It stood at US$172/t (-17% month-on-month and -77% year-on-year), the lowest level since August 2023. However, the dairy herd remains large, and milk production continues to be strong, reaching 8.99 million tons (+3.2% or +279,000 tons vs. 2025). US raw milk prices remain under pressure, at US$41.89/100 kg (-7.9% vs. December 2025 and -27.4% vs January 2025).

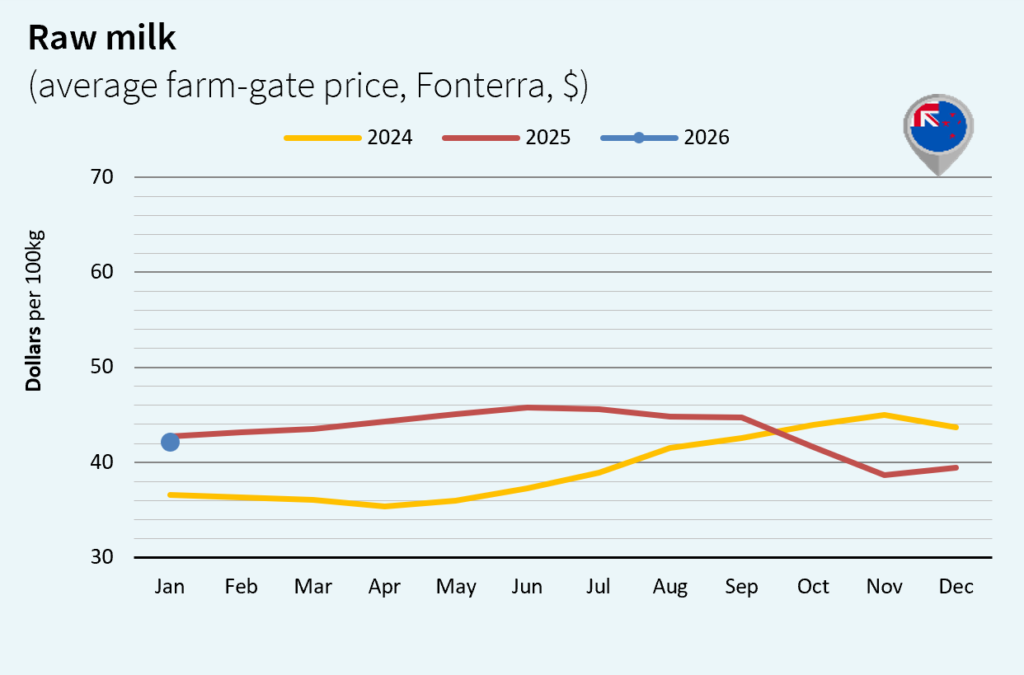

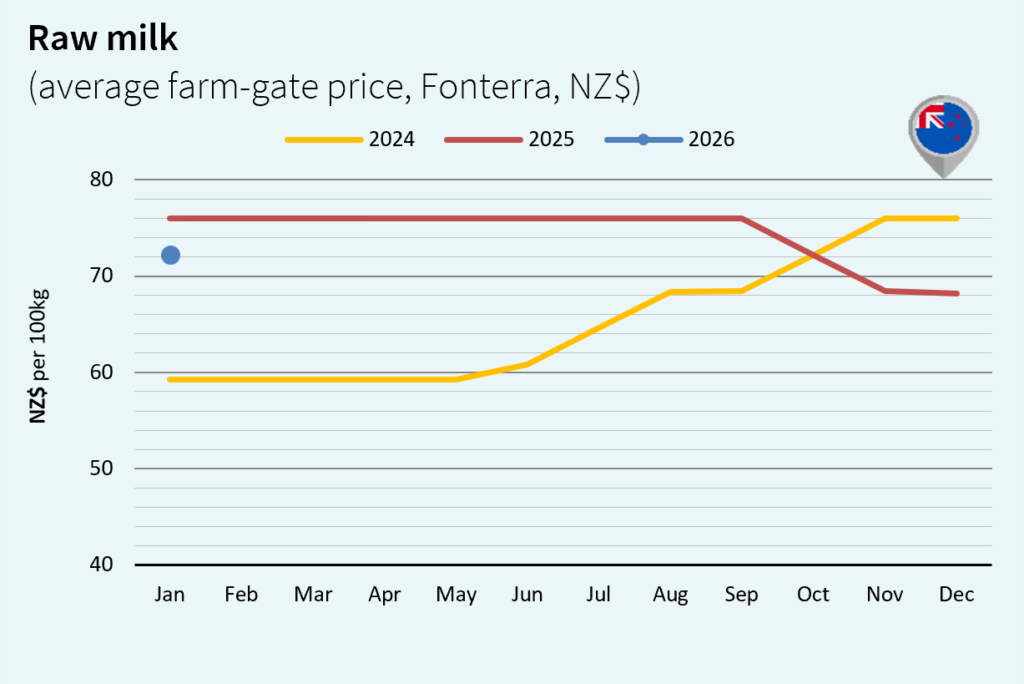

Why is New Zealand showing recovery in milk prices?

After the seasonal milk peak, pasture availability remained high in January 2026. Milk production exceeded 2.43 million tonnes (+2.0% or +47,000 tonnes vs. 2025). After months of decline, dairy commodities prices began to rebound with buyers expecting prices to have bottomed and purchasing to cover short forward positions. The conflict in Iran is expected to support this trend in the coming weeks. NZ raw milk price recovered to US$42.18/100 kg (+7.0% vs. December 2025 and -1.4% vs January 2025).

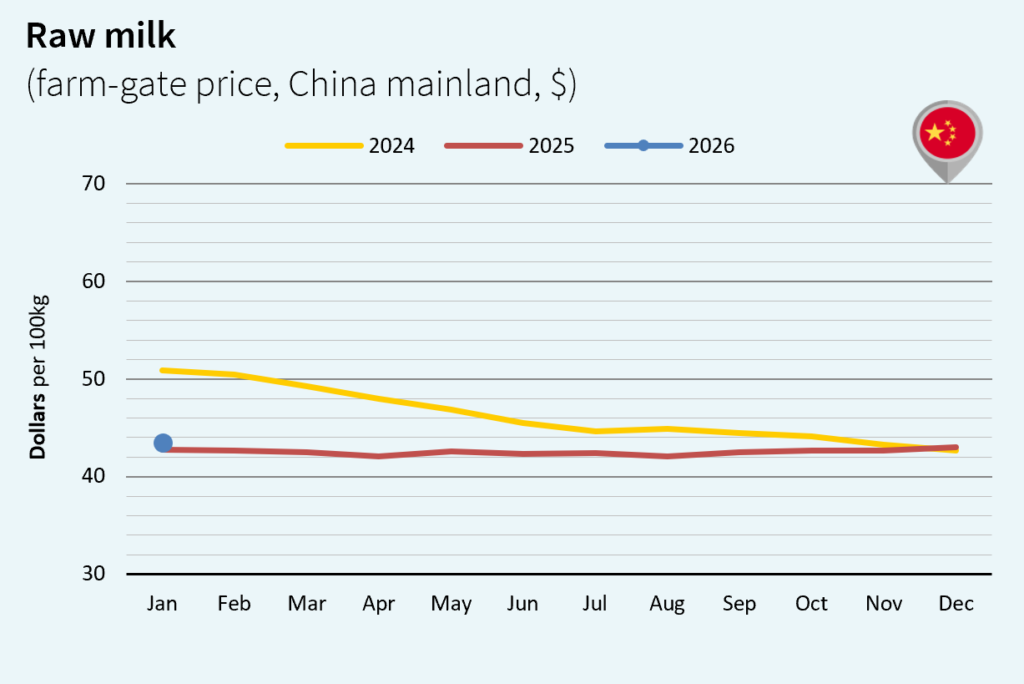

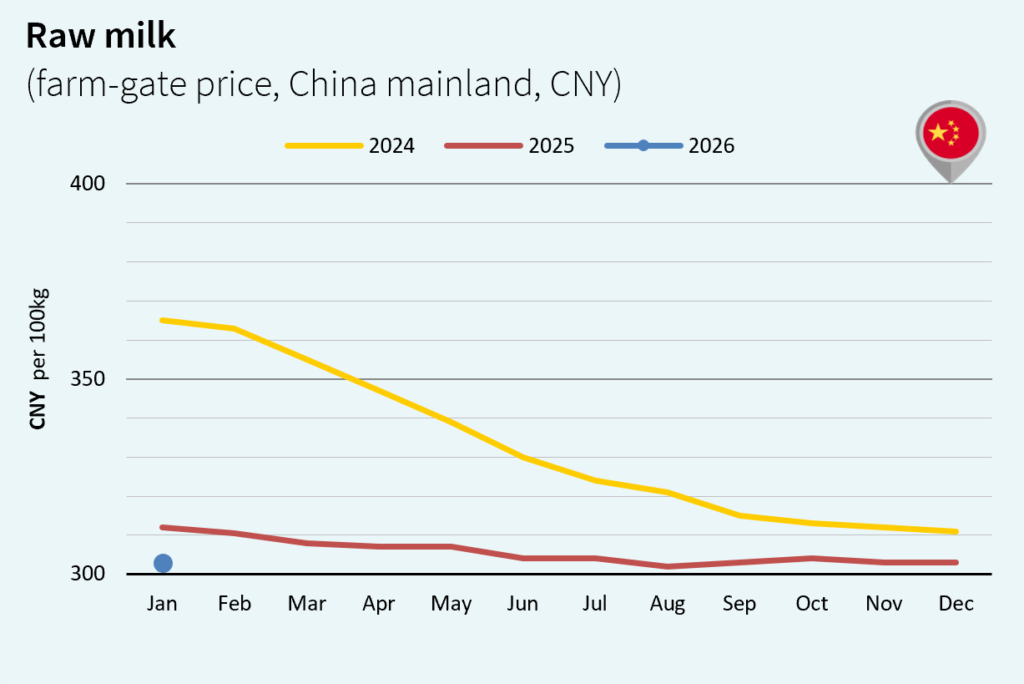

What are the current trends in China’s dairy sector?

The Chinese dairy sector continues its long economic recovery. Chinese farmgate milk prices have been on a sustained downward trend for several years, pushing smaller farms out of the market or into consolidation with larger players. Now, seasonal production eases and holiday-driven demand strengthens market balance. Chinese domestic dairy demand remains steady overall but import ingredient demand recovery is uneven by product. The Chinese raw milk price held steady in local currency but increased in US dollars, reaching US$43.48/100 kg (+1.1% vs. December 2025 and +1.7% vs January 2025).

Source:

![]()