02 Mar 2026

Share on:

What does the Milk Market Outlook for January 2026 show?

What was the global trend in milk production?

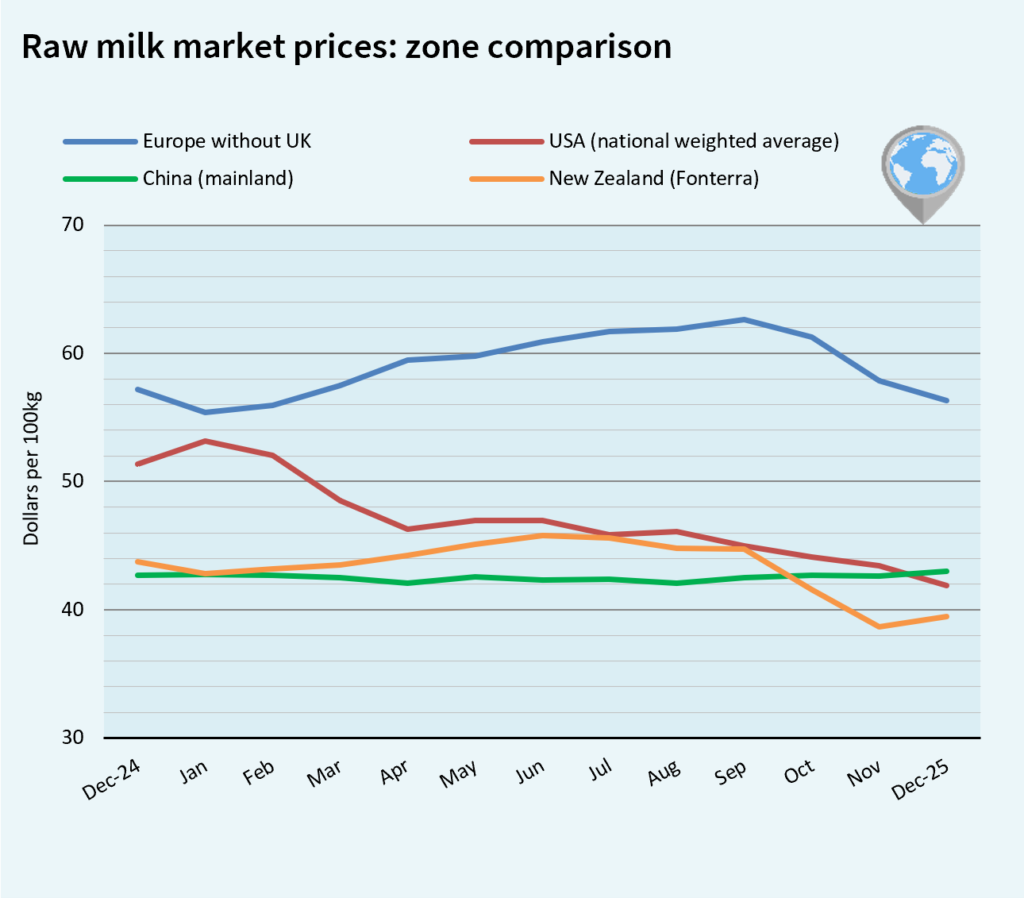

The Milk Market Outlook January 2026 analyzes December 2025 data, highlighting continued growth in milk production across major exporting regions and sustained pressure on raw milk and dairy commodity prices. While supply expanded in the EU, U.S., and New Zealand, global price dynamics remained constrained by abundant availability and fragile demand in key markets such as China.

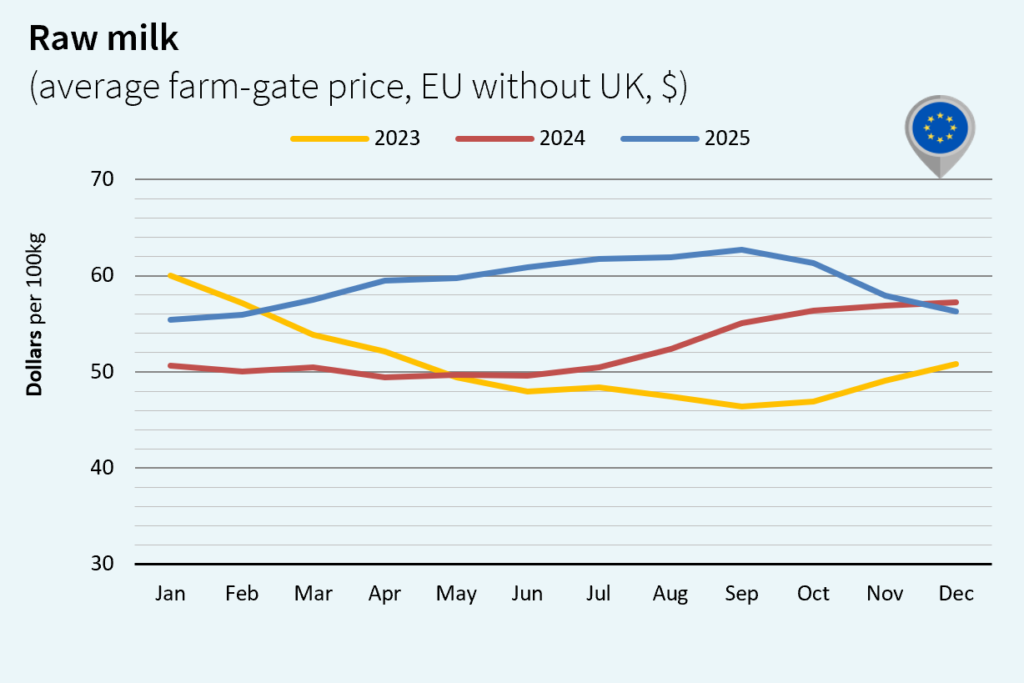

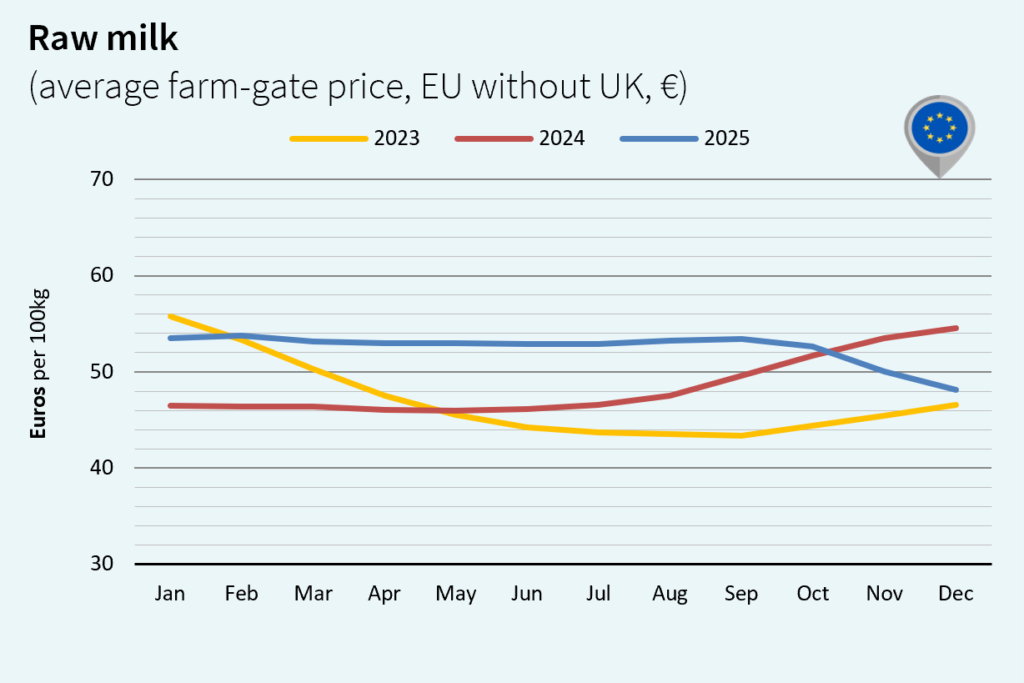

How is milk production evolving in the European Union?

December 2025 milk deliveries among the main European exporters were trending upward, except in Ireland (-3.0% vs. 2024, at 267,000 tons). With a clear rebound in production, EU-27 exports recorded marked increases over the last quarter. However, current supply levels are weighing on price. On average, EU price stood at US$56.31/100 kg (-2.7% vs. November 2025 and -1.5% vs. December 2024).

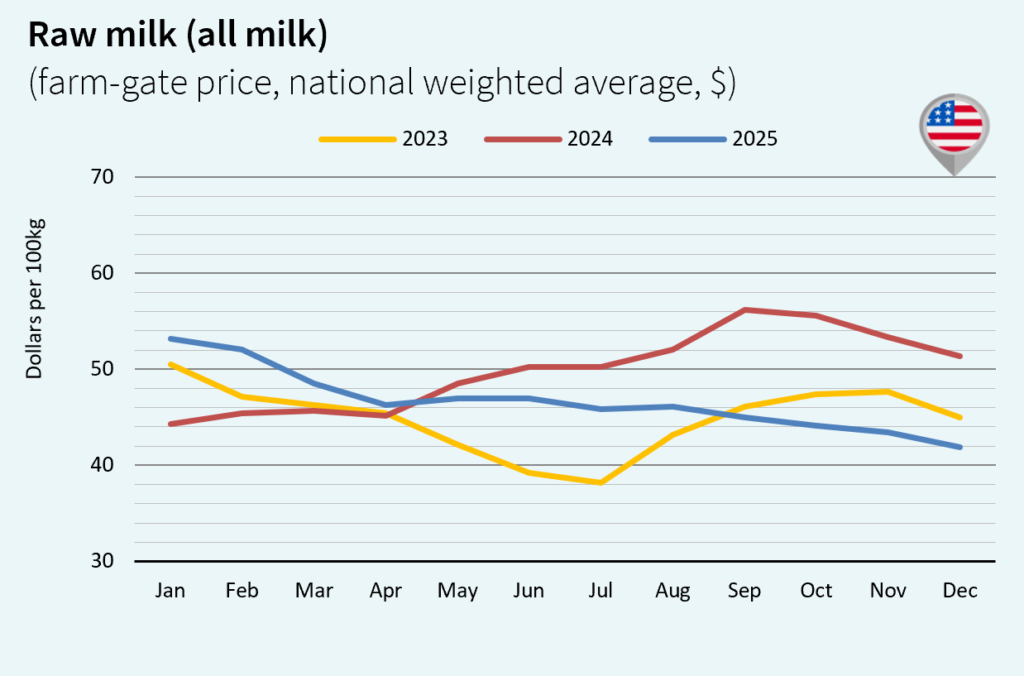

What is driving milk production and prices in the United States?

In the US, milk production remained strong despite tighter margins. December 2025 country’s output increased year-on-year by 374,000 tons, reaching 8.88 million tons (+4.5%). Despite a clear rebound in exports, the additional production is weighing on prices. The U.S. butter quotation continued to trend downward, remaining well below the €3,000 per ton mark. The same applies to raw milk, at US$41.89/100 kg (-3.6% vs. November 2025 and -18.5% vs. December 2024).

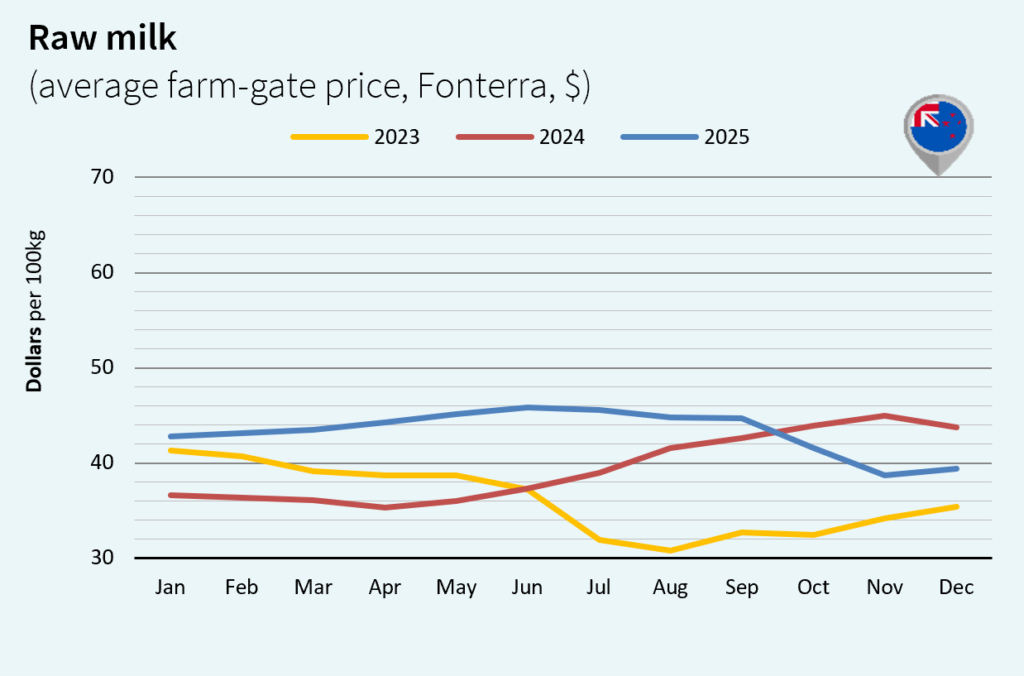

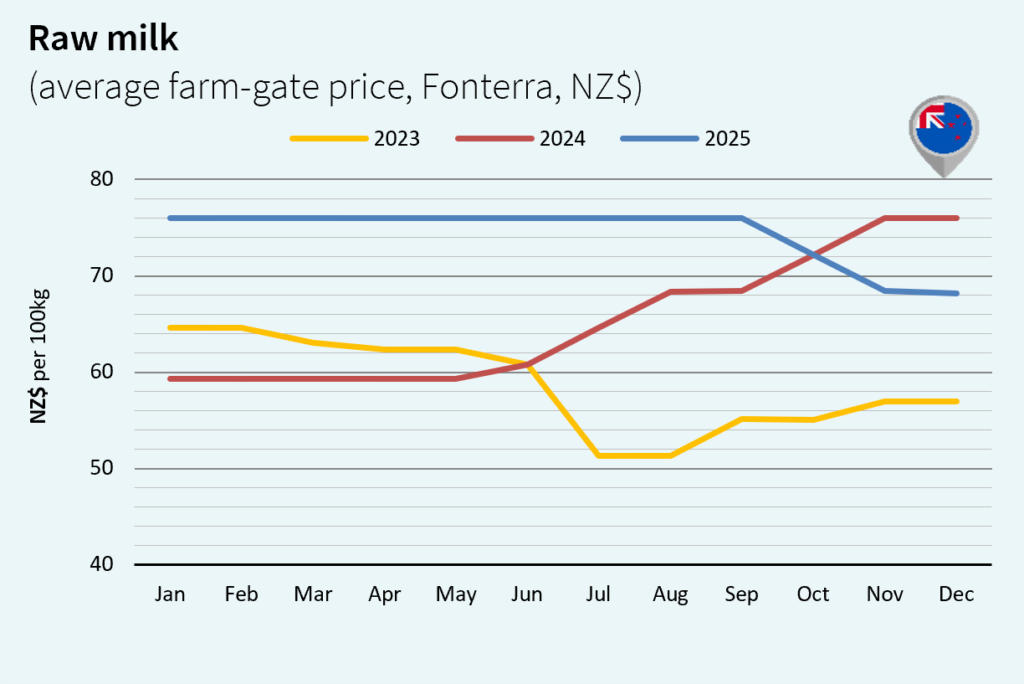

Why does New Zealand maintain strong milk production despite price pressure?

In New Zealand, milk production remains strong, supported by generally favorable weather conditions. December 2025 production increased again by 65,000 tons to reach 2.71 million tons (+2.5% vs. 2024). However, the rise in milk and dairy product supplies elsewhere around the globe is also weighing on New Zealand prices. Nevertheless, NZ raw milk price increased in US dollar terms due to the appreciation of the NZ dollar. It reached US$39.44/100 kg (+1.9% vs. November 2025 but -9.8% vs. December 2024).

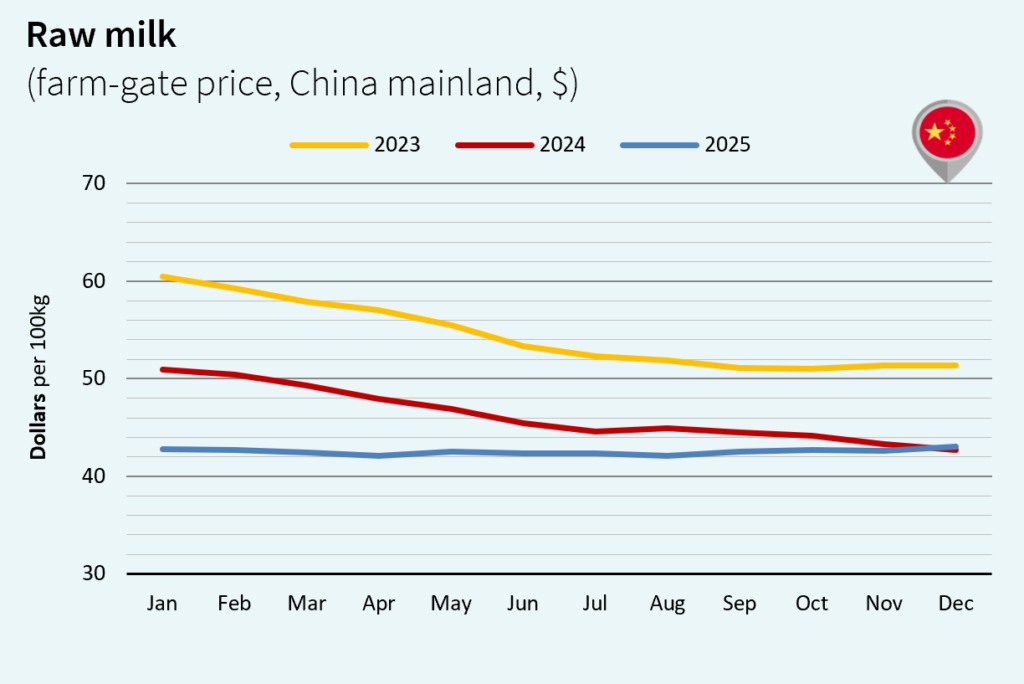

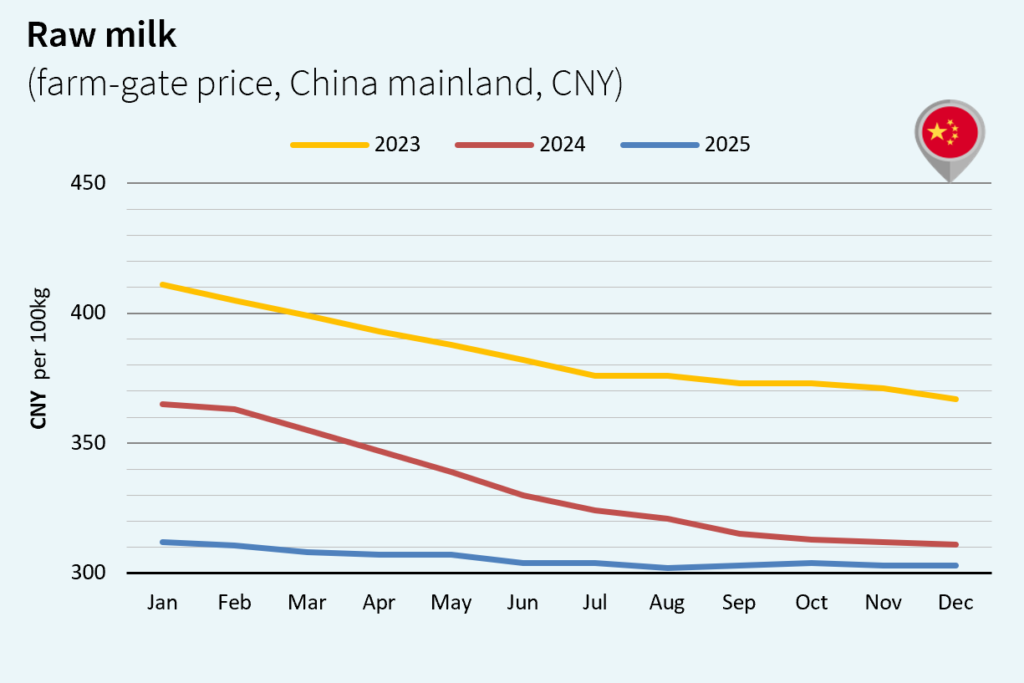

What challenges is China’s dairy sector facing?

The Chinese dairy sector has not yet recovered from the crisis and remains fragile. Domestic raw milk prices remained under pressure as the global economic environment deteriorated. December 2025 Chinese raw milk price held steady in local currency but increased in US dollars, reaching US$43.01/100 kg (+0.9% vs. November 2025 and +0.7% vs. December 2024). China set tariffs on EU dairy products (cream and cheese) at 7.4%-11.7% in its final ruling, instead of the 21.9%-42.7% initially imposed. EU producers may struggle to compete with the New Zealand industry in accessing the Chinese market in 2026.

Source:

![]()