04 Jun 2026

Share on:

Beef Market Outlook (Baptiste Buczinski)

Welcome to the Beef Market Outlook May 2026, your monthly overview of global beef markets and pricing trends. This edition reviews data from April 2026, examining recent developments in beef production, cattle pricing, and export activity across Europe, Brazil, China, and the United States. Through clear, data-led insights, we outline the main drivers shaping global supply and demand, trade flows, and overall market performance.

Which global beef price signals stand out in May 2026?

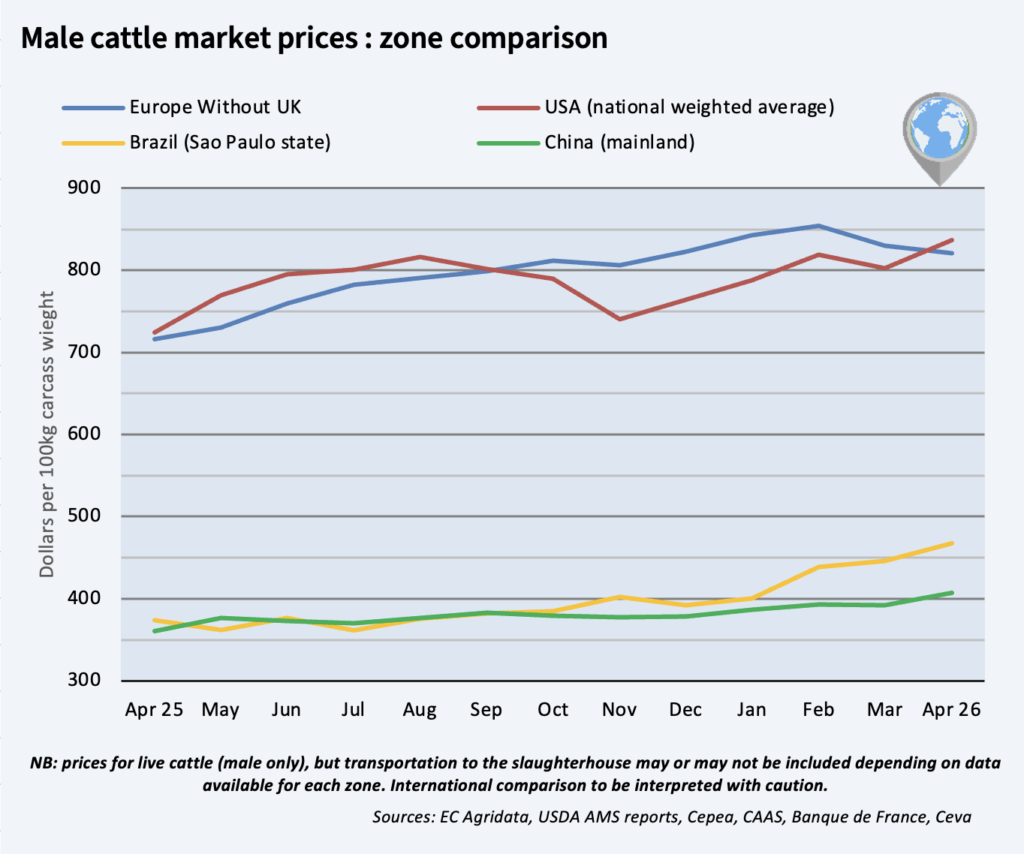

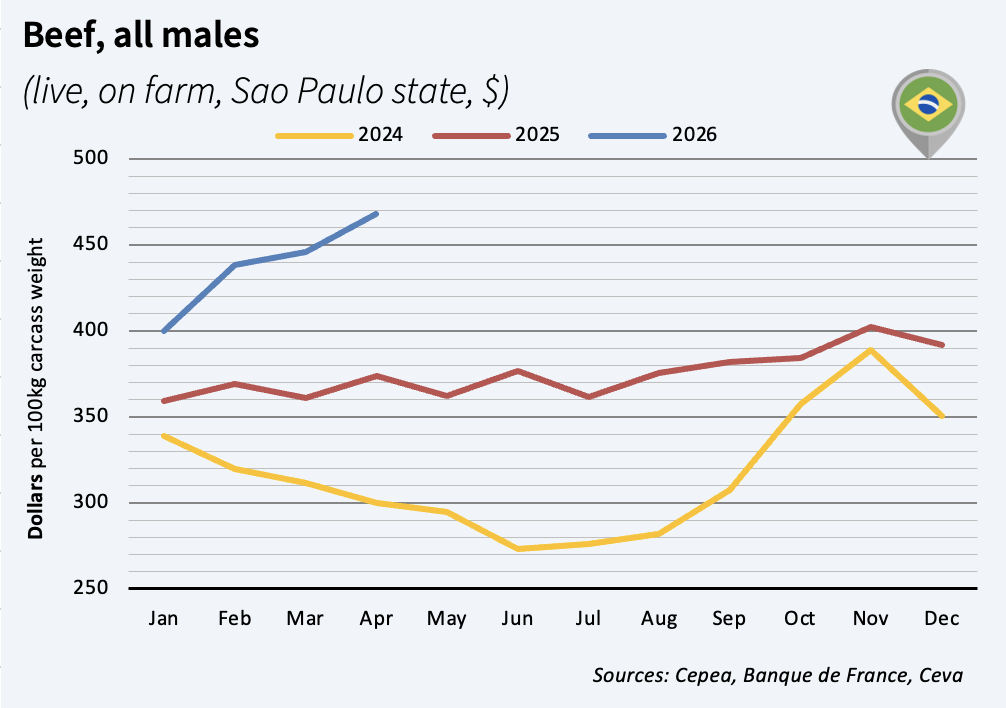

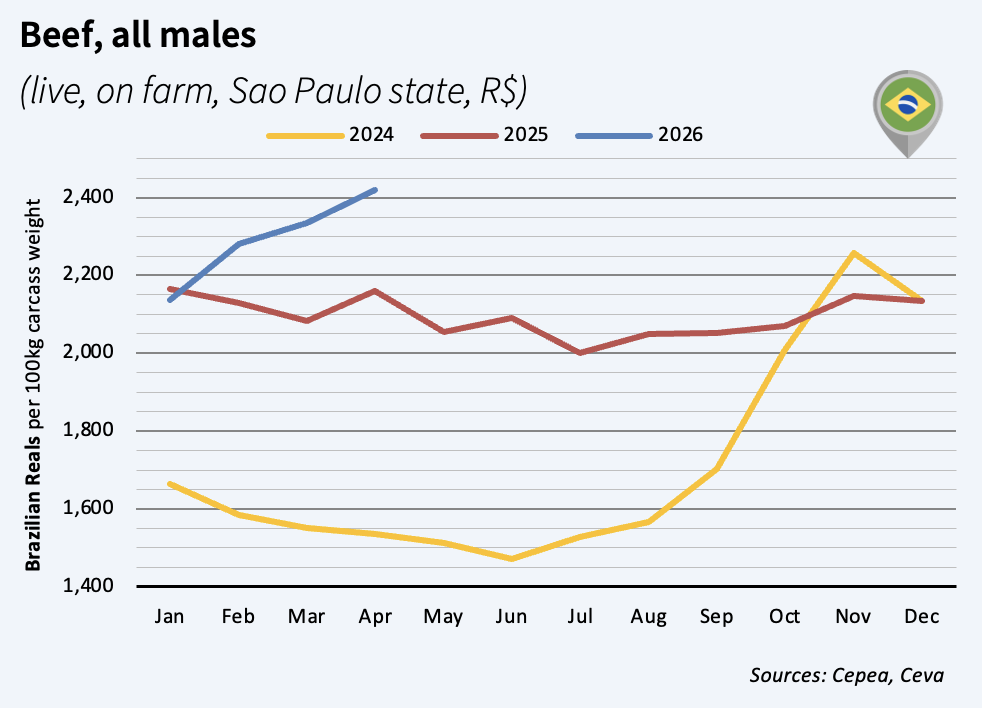

In April, Brazilian prices went quickly up as World demand is strong, with low inventory numbers in Europe, USA and China. European male prices decreased, as consumers are eating a bit less beef.

Why are European cattle prices easing but still above last year’s levels?

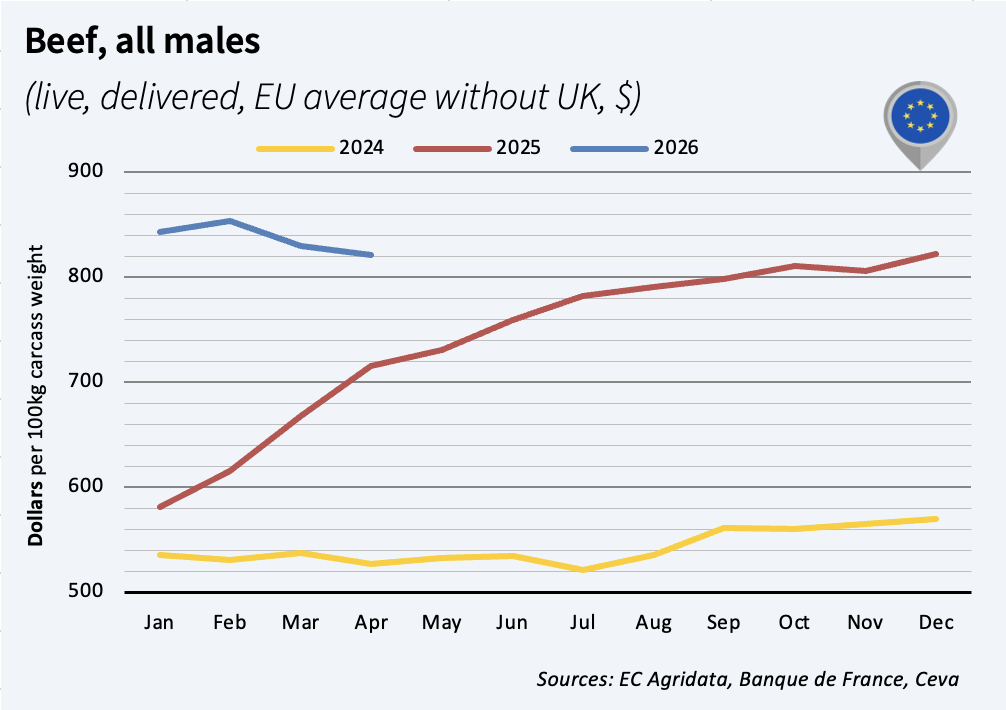

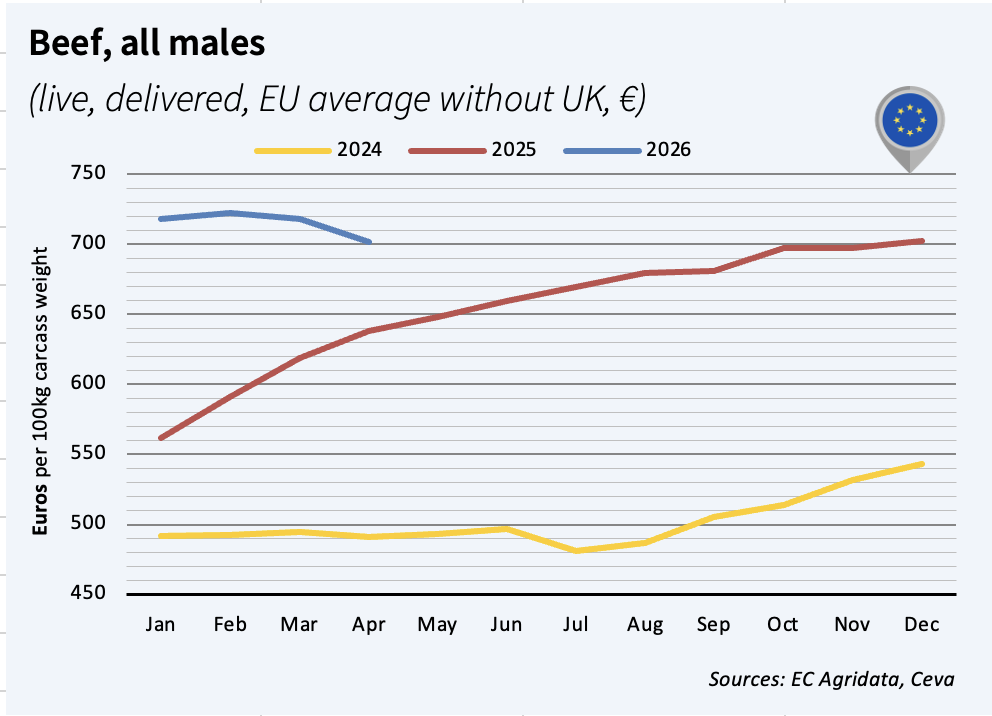

In April, male carcass prices fell 1% month‑on‑month (USD) in Europe but remained 15% above 2025 levels. Prices are easing seasonally with the approach of summer, while high consumer beef prices and the Middle East conflict are slightly dampening demand. Cattle slaughter also continued to decline in Jan–Feb 2026 (-5% year‑on‑year).

How are tight cattle supplies reshaping the US beef market?

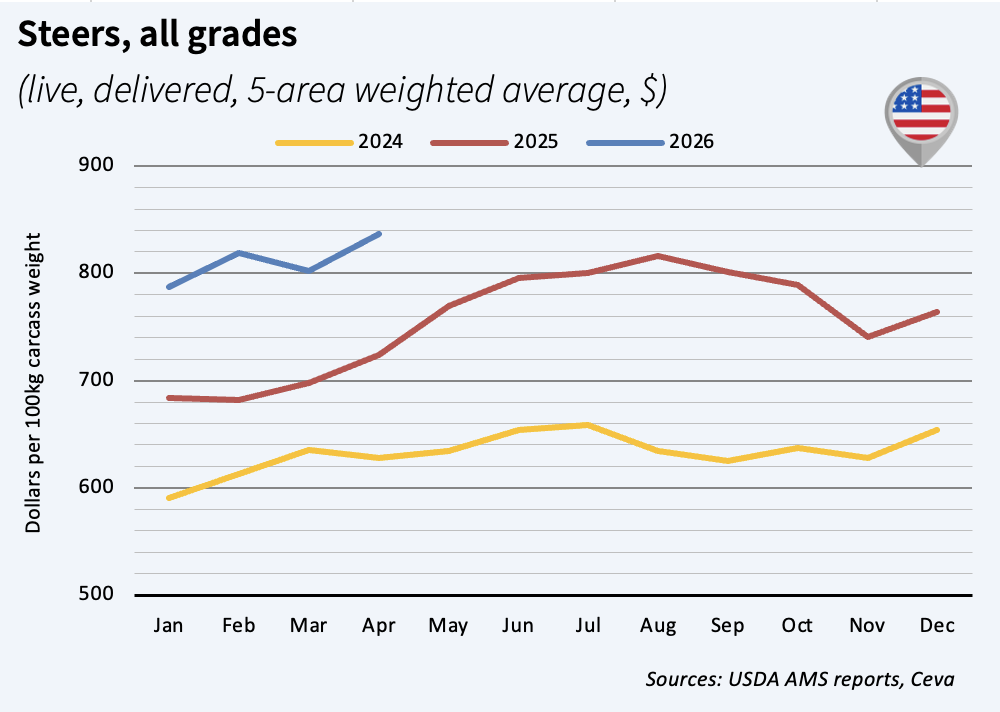

In April, steer prices rose 4% month‑on‑month and remained 16% above last year’s record. A seven‑year decline in herd size (2020–26) has supported prices, though the cycle could shift as more heifers have been retained since January. Poor pasture conditions in May—the worst since the 2021–22 drought—continue to constrain supply. Slaughter remains weak, driving a 15% rise in US beef imports in Q1 2026 (notably from Mexico, Australia and Brazil), while exports fell 18% year‑on‑year.

Why is Brazil strengthening its position in global beef exports?

Brazilian beef prices rose 5% month‑on‑month, reaching 25% above 2025 levels (USD). Exports totaled 1.28 million cwt in Jan–Apr 2026 (+14% year‑on‑year), with April marking a record for that time of the year. Shipments of 618,000 cwt to China and Hong Kong led the growth (+19%), despite China capping duty‑free imports at 33% below 2025 levels. Exports also increased to the US (+10% y-on-y), other North America (+12%), Egypt (+46%) and the EU (+23%, 42,000 cwt), while remaining stable to the Middle East. In April, exports focused more on China and the EU, declining to other regions.

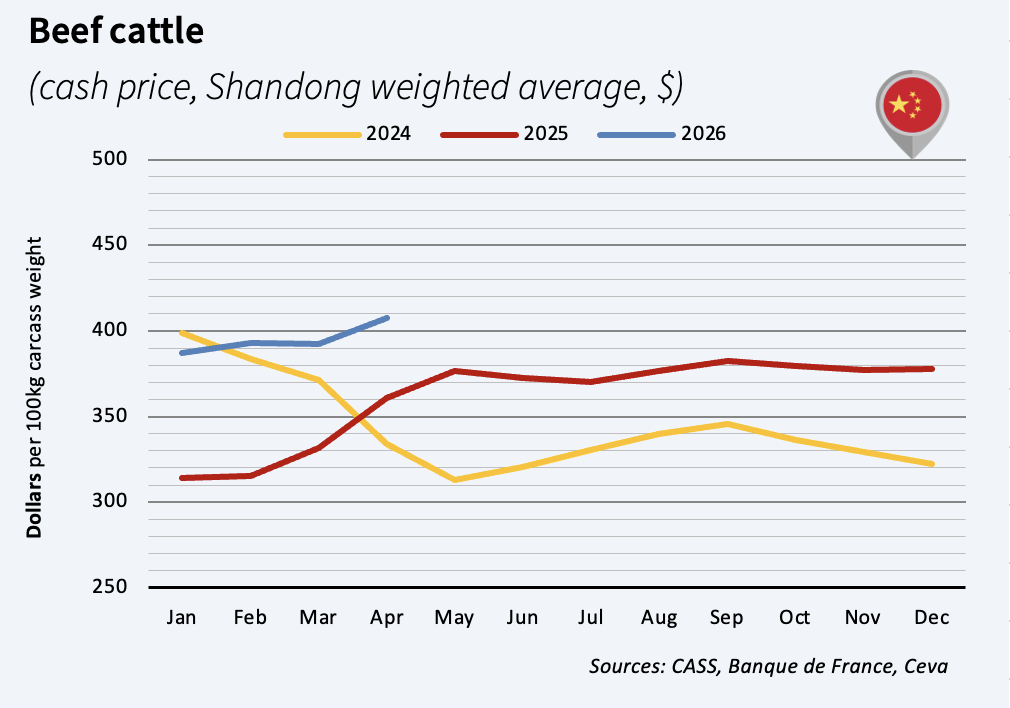

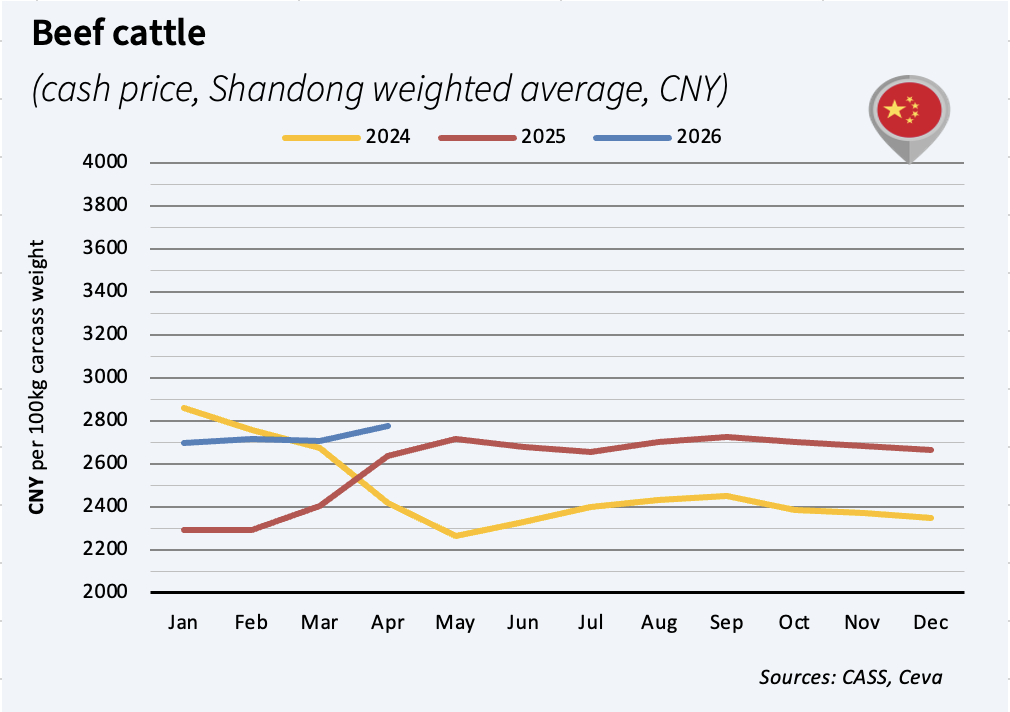

How are China’s imports influencing the beef market in May 2026?

Beef prices rose 4% month‑on‑month, supported by signs that China’s herd contraction (-6% in 2025) is stabilizing the market. In April, China imported 795,000 tons cwe in Q1 2026 (+6% year‑on‑year), with growth driven by Brazil, Argentina and Australia. In April, Brazil notably increased shipments to China by 27% year‑on‑year.

Source:

![]()